Should I stop paying into my pension if it exceeds the Lifetime Allowance?

Monday 28th June, 2021

"Should I keep paying into my pension if it reaches the Lifetime Allowance"

This is a question I am frequently asked by clients who are approaching (or have exceeded) the pension Lifetime Allowance threshold and are concerned that they may trigger a 55% tax charge on their pension.

This is a very valid concern, but for many people, the implications of exceeding the Pension Lifetime Allowance are not as horrendous as they may think and there may be far more benefit in continuing to fund their pension.

In the article below I will discuss the various options available when the Lifetime Allowance is exceeded. I will also highlight through calculations and examples, circumstances in which it is potentially better to continue funding your pension.

The Lifetime Allowance (LTA) is the maximum amount of benefits a person can build up in pensions (Defined Benefit and Defined Contribution) over their lifetime. If pension benefits exceed the LTA, they can trigger a Lifetime Allowance charge on the excess of up to 55%. The LTA currently stands at £1,073,100.

Now, this wasn’t a problem for most people, when the LTA was at the lofty heights of £1,800,000 in 2011/12. There wasn’t much impact when it was reduced down to £1,500,000 in 2012/2013 or even further to £1,250,000 in 2014/15. However, a reduction down to £1,000,000 in 2016/17 brought many middle-income earners with final salary schemes or carefully built-up money purchase schemes into the remit of the LTA charge. All you need was a final salary pension offering an income of over £50,000 per year and you were in excess of the LTA.

As a result of this, I have seen a noticeable increase in the number of people who are either:

- Rapidly approaching the LTA and are wondering if they should move into cash and stop contributing to their pension

- Have already exceeded the LTA and are wondering if it is still worth contributing to their pension

This is a really difficult question to answer in many ways, but I think the starting point to consider, is that the aim of this type of legislation is not to be punitive. It is put in place to reclaim a benefit you weren’t entitled to and to put you in the position you would have been in if you hadn’t received it. The end result of any of these types of charges is not as dramatic as everybody suspects, when you look at it closely.

Before we carry on to the crux of the question, it is important to lay some groundwork and clarify a few misconceptions. So, in the next few paragraphs, we will review the Lifetime Allowance and some of it’s working, look at some of the alternatives to saving into a pension and then look at whether it is better to keep saving into the pension or rather to stop all contributions. We will also consider whether you should move into cash, in order to avoid exceeding the Lifetime Allowance.

What triggers a test against the Lifetime Allowance?

This is a very important question to answer, because many people labour under the misconception that simply exceeding the LTA triggers a test and potential LTA charge on the excess. This is simply not the case. The LTA charge is only triggered when the benefits in excess over the LTA are crystallised. Your benefits are crystallised as a result of a number of things, but the main crystallisation events are:

- When you start to take your benefits

- Reaching the age of 75

- Death

The key way that pensions are normally crystallised is when you start to take your pension benefits. By controlling how you crystallise your benefits, they can be crystallised incrementally, with crystallised and uncrystallised pension benefits residing together in the same pension wrapper.

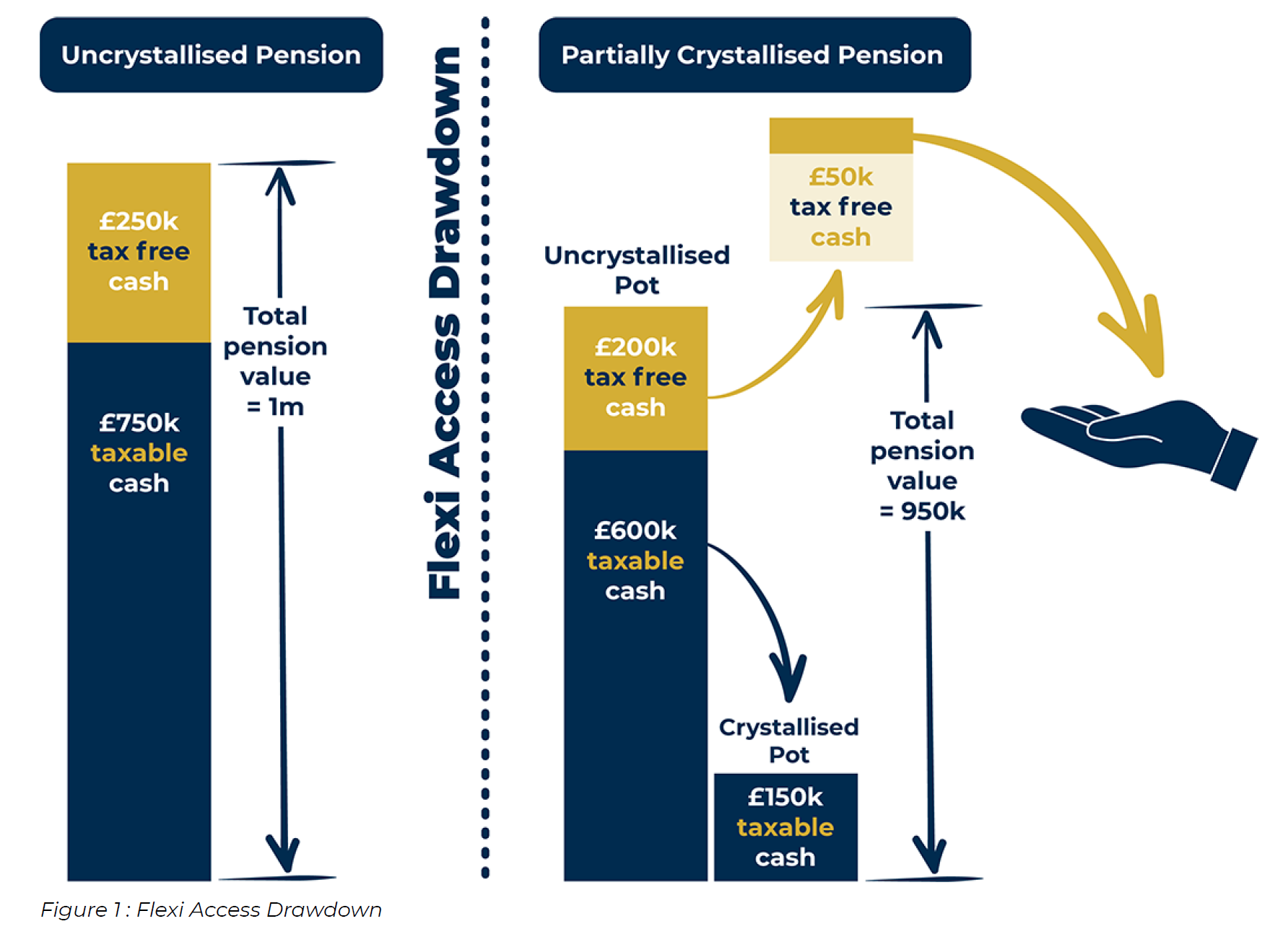

This is demonstrated in the diagram below. As you can see, prior to crystallisation the pension member has a total pension of £1,000,000. Of this, £250,000 (or 25% of £1m) can be taken as a tax-free lump sum. The member decides that they want to withdraw £50,000 as a tax-free lump sum. In order to do this, they need to crystallise £200,000 of their pension (£200,000 x 25% = £50,000). The £50,000 is paid out to the member as a tax-free lump sum. The remaining £150,000 of the now crystallised pension pot remains within the pension, alongside the remaining £800,000 uncrystallised pot (of which £200,000 can still be taken as a tax-free lump sum).

The key takeaway from this is that it is possible to delay triggering the LTA, by crystallising all your pension up to the available limit and leaving the excess uncrystallised. Now this is harder to do with Defined Benefit (Final Salary) pensions, but if you have a bog-standard money purchase scheme, then you actually have far more control over the timing of any future LTA charge than you realised.

For example, Mr. Ortega has a pension worth £1,500,000. He does not wish to immediately trigger the LTA charge, so he crystallises £1,073,100 of his pension, leaving the excess over this limit (£426,900) uncrystallised. As the excess over the LTA has not been crystallised, it will not trigger an immediate LTA charge.

How is the Lifetime Allowance charge calculated?

Now many people assume that the LTA charge will be 55% on the excess over the Lifetime Allowance. However, this is simply because that is what the media chose to focus on. The reality is that most people, simply through the options they choose will more likely pay the lower charge of 25%.

So, if you crystallise more than your available LTA, the excess over the limit will be subject to tax at:

- 25% if you leave the excess in the pension, as pension benefits. However, you remain liable for income tax on any income received after the 25% charge is paid

- 55% if you withdraw the excess as a lump sum

The question arises, when would you take the excess out as a lump sum? Some people may need it to off a debt or a mortgage. Or else, they may want to make a gift of the residual lump sum to one of their children or some other loved one.

However, apart from really isolated situations, I cannot see a reason why you would opt for taking the money out of the pension. The reason for this is as follows:

- Firstly, you are going to pay a 55% charge on the full amount

- Secondly, while them money remains within the pension wrapper, it is free to grow in a tax-free environment, thus allowing the possibility for greater growth. If you take it out of the pension with the aim of investing it, you are going to pay tax on any returns, unless you invest it all into an ISA

- Thirdly, while the money remains in the pension it generally does not form part of your estate for Inheritance Tax purposes and can be left to anyone of your choosing upon death. If you take it out of the pension, you bring the money into your estate, where it will be subject to Inheritance Tax. You could gift it away immediately and it would probably qualify as a gift out of excess income, but it seems a bit counterintuitive to crystallise a 55% charge simply to gift it away.

I spent a bit of time working out the effective tax rate of crystallising the excess over your Lifetime Allowance. This assumes that the contributions to the pension were made initially from pre-tax income by the employer, free from National Insurance or tax. The results are below:

Take excess as a lump sum

If you take the excess out as a lump sum, the effective tax rate is 55%, regardless of your personal tax status at the time.

Leave excess as pension and draw it out as income

Here we assume the excess is crystallised, but left as pension, to be drawn out as income. A 25% charge will be paid on the excess and income tax will be paid on the excess at the member’s marginal rate. The effective rates are laid out in the table below:

|

Tax status |

Effective tax rate |

|

Additional Rate Taxpayer (45%) |

58.75% |

|

Higher Rate Taxpayer (40%) |

55% |

|

Basic Rate Taxpayer (20%) |

40% |

|

Non-Taxpayer (0%) |

25% |

The table above obviously does not take account of situations where the income pushes the recipient into a new tax bracket, so that some of the income is taxed at one level, while the rest is taxed at another.

As you can see from the above, if we look at this purely from the perspective of the impact of Income Tax, then the Additional rate taxpayer will be better off taking the excess out of the pension as a lump sum, while the Higher Rate Taxpayer will be in a fairly neutral position. Basic Rate and Non -Taxpayers are better off leaving the money in the pension and drawing it out as income.

This however does not take consideration of the impact of Inheritance Tax and the benefit of keeping the pension in a tax-free environment.

It is also important to remember, when trying to avoid the LTA charge, that the charge is paid from the pension funds. You don’t have to personally write out a cheque to pay the liability. Therefore, you are never going to be in a position where you are scrambling to find the funds to meet the liability.

What are the alternatives to pension contributions?

The next question to consider is, “What are the alternatives to pension contributions?”

I have discussed some of the alternatives below:

Cash allowance

According to research by the LCP consultancy, 84% of FTSE100 companies offer a cash alternative to pension contributions (Pension Age, 84% of FTSE 100 firms offer a cash alternative to pensions – LCP, 11/05/2017) for employees that have breached the LTA or Annual Allowance.

This generally allow the employee to opt to receive the contribution that would have been made into their pension, as income. This is subject to Income Tax, employee National Insurance and is also reduced to make provision for the employer’s 13.8% National Insurance contribution.

The effective rate of this for a Higher Rate Taxpayer is therefore approximately 55.8% and 60.8% for an Additional Rate Taxpayer. The addition of the 13.8% employer National Insurance payment to the mix, makes this a pretty unattractive option.

If you were to adopt this option, you would probably look to utilise this option to do something to provide for the future. This would generally involve saving into an Investment ISA in order to build up an investment pot that could grow in a tax-free environment and also could generate a tax-free income in the future. Alternatively, you could make contributions to Enterprise Investment Schemes (EIS) or Venture Capital Trusts, that could provide an immediate tax relief of 30% to reduce Income Tax. The returns from these investments also tend to be tax free, provided relevant requirements are met. Where these fail as a solution is that they are inherently risky investments and also lack liquidity.

Stop funding your pension

In the absence of a cash allowance option, another alternative is to stop funding the pension altogether. This seems completely counterproductive, particularly if a large proportion of your pension contributions are made up of employer contributions.

To demonstrate this, let’s look at what HSBC offers UK staff via the UK Future Focus Scheme:

HSBC contributes the following:

- 10% of the employees first £22,100 pensionable salary

- 9% of anything over £22,100 up to the scheme earnings cap, currently £150,000

- Plus, HSBC will match anything the employee pays up to 7% of their pensionable salary up to the scheme earnings cap, currently £150,000

Not too bad, huh? Anyway, what does that look like in reality? Let’s say an employee has a pensionable salary of £35,000. They make the full 7% contribution to their pension. They will receive the following annual contribution:

|

10% of first £22,100 |

£2,210 |

|

9% of the next £12,900 |

£1,161 |

|

7% employee contribution |

£2,450 |

|

7% matching employer contribution |

£2,450 |

|

Total Employer contribution |

£5,821 |

|

Total employee contribution |

£2,450 |

Therefore, in return for a contribution of £2,450, the employee is getting a return of £5,821. If we reduce that to take account of a maximum LTA charge of 55%, the employee is still getting £2,619.45 in return for their £2,450 contribution. This does not include the tax-free growth achieved by these funds while invested, or the fact that it is outside of the estate for Inheritance Tax purposes.

Based on the above, it is quite clear that it is not in the employee’s interest to give up the contributions to the pension completely, simply because the LTA has been or is likely to be exceeded.

There are numerous other possibilities here, but I have chosen the most common which is the person funding their pension from their pre-tax salary.

Should I take the cash allowance and fund an ISA?

This was an interesting calculation to work out. I used a compound interest calculator in order to figure out the returns. I used a 5% annual return and assumed that the employee continues to contribute to the pension for 10 years. I assumed that the employee’s pension already exceeds the LTA, so all contributions and any growth will eventually be subject to an LTA charge. The final outcomes will naturally vary depending on how you calculate the interest etc. However, the below is simply fore illustrative purposes.

I assumed that the amount being contributed to pension was £20,000 and the employee has the option to either contribute this straight into his pension or take the cash allowance alternative, paying Income Tax, as well as employer and employee NI.

The net contribution that the employee would make to their ISA each year would be £8,840.

Should the employee opt to continue paying the £20,000 into their pension, then the gross contribution each year would be £20,000.

- After 10 years, the ISA would be worth approximately £111,188.00.

- After 10 years the pension would be worth approximately £251,557.00.

So far it is all looking rather positive for the pension. However, there is still the Lifetime Allowance charge to be deducted, while there is no further tax to pay on the ISA.

If the employee decides to take the excess as a lump sum, they will pay a 55% LTA charge (£138,356). This will leave them with a lump sum (net of the LTA charge) of £113,200. This is notionally slightly better than the ISA, but in reality, it is very much the same outcome.

If the employee was to leave the excess in the pension and draw the funds out as an income in the future then the outcomes very much depend on the employee’s tax status at the point that the withdrawals from the pension are made. This is demonstrated in the table below:

|

Tax Status |

Net of 25% LTA charge |

Net of Income Tax |

Total LTA charge and Income Tax paid |

|

Additional Rate |

£188,667.75 |

£103,767.26 |

£147,789.74 |

|

Higher Rate |

£188,667.75 |

£113,200.65 |

£138,356.35 |

|

Basic Rate |

£188,667.75 |

£150,934.20 |

£100,622.80 |

|

Non-Taxpayer |

£188,667.75 |

£188,667.75 |

£62,889.25 |

As you can see, there is no difference in terms of the LTA charge. They all pay the 25% LTA charge at the point that the benefit is crystallised. However, the income tax status makes a considerable difference. As highlighted earlier, the Additional Rate taxpayer is worst off, with net receipt of £103,767.26. This is approximately £7,420 worse off than if the cash allowance had been taken and invested in an ISA.

All the other tax statuses are better off (if only slightly) than if the cash allowance had been taken. Now, this calculation does not take into account the fact that you would be drawing these incomes down over years and all the time, they would be generating more growth. However, this would also be the case with the ISA, and if we assume that they are invested similarly, then it is fine to discount this.

However, the ISA will still be subject to Inheritance Tax upon death, so it may still be far more beneficial to build up the funds in the pension, rather than take a cash allowance and save into an ISA.

All of this goes to support my initial statement, that the LTA charge does not have as dramatic an impact as we were all initially led to think, and is not punitive. Either way you receive the funds, you would have had to pay some sort of charge, either via tax, National Insurance or the Lifetime Allowance Charge.

Should I move into cash to stop my pension growth taking me over the Lifetime Allowance?

This is relatively easy to answer. My view is that halting growth on your pension to avoid paying an LTA charge makes very little sense at all. The only reason you would do this is because you resent the idea of paying an LTA charge to HMRC to such an extent that you are willing to give up returns for the privilege of avoiding doing so.

Let’s use an example to illustrate my point. Your pension is £1,000,000 and you move into cash in order to avoid your pension exceeding the Lifetime Allowance. You move into a cash account that generates 0.5% per annum. After 2 years, you end up with approximately £1,010,025.

Alternatively, you leave your pension invested and have two moderate years of 5% per annum. Your pension is now worth £1,102,500. You have therefore exceeded the LTA (£1,073,100) by £29,400. Let’s say that you automatically crystallise all your pension at that point and withdraw the excess as a lump sum, you will pay £16,170 (£29,400 x 55%) on the excess over the LTA. Net of the LTA charge, you would be left with £1,086,330. This is considerably better than the result if you move the funds into cash.

It therefore does not make sense to move into cash in order to avoid exceeding the LTA charge. Rather pay a charge in return for greater overall returns, than avoid a charge, by consciously taking steps to end up poorer.

It is also important to remember the fact that the charge will be paid out of the pension funds, so paying this liability is going to be relatively straight forward. It therefore makes sense to maximise your returns, even if you only get to keep a portion of them.

Final Thoughts

I hope this article provides some clarity on what appears to be quite a confusing and scary area for many. While it is always important to take some advice on these areas, the figures in the articles highlight that the impact of the Lifetime Allowance charge is not as dramatic as we generally think. We can still achieve relatively good result from pension contributions.

However, there are circumstances and situations where it can make no sense whatsoever to continue contributing to your pension. It is therefore worth running your position past a good financial adviser who can talk you through the steps to ensure that the options you choose are appropriate and in your best interests.

If you have any questions or would like to discuss this further, please don’t hesitate to give us a call.